Every calculator request and lender click-out since inception, distilled to the five features that decide where Bitcoin borrowers go: custody, payment structure, term, fees, and rate design.

By Steven Han and Michael Song, Co-Founders of Borrow on Bitcoin · July 14, 2026

Ask a lender what Bitcoin borrowers want and you will get a pitch. Ask the borrowers and you get answers. Since the borrow/on/bitcoin calculator went live in May, we have collected information on the features borrowers ask for most.

A note on method up front: these are revealed preferences, not survey answers. We map each click-out to the published attributes of the product chosen (custody model, payment structure, term, fees, rate design) from our lender directory, verified weekly. Bots, which accounted for nearly half of raw clicks, are filtered out. The full methodology sits at the end.

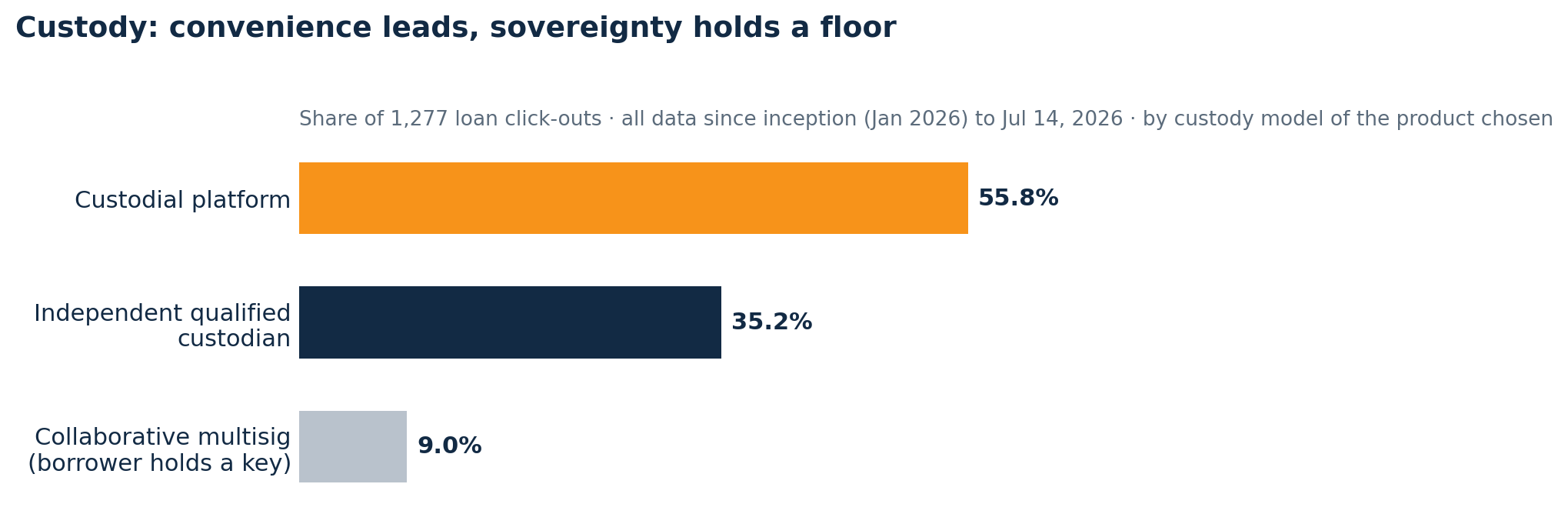

Custody: convenience leads, sovereignty holds a floor

A slim majority of demand, 56% of click-outs, goes to products where the lender holds collateral on its own platform. Another 35% goes to products that park collateral with an independent qualified custodian. Collaborative multisig, where the borrower keeps one of the keys, holds a durable 9% floor.

The sharper line is not who holds the keys but what may be done with them. Products whose terms state that client collateral is not re-lent captured 96.5% of demand. The one product in the set whose standard terms permit rehypothecation drew under 4% of clicks. Borrowers will tolerate a custodial platform; they will not tolerate their coins being lent out.

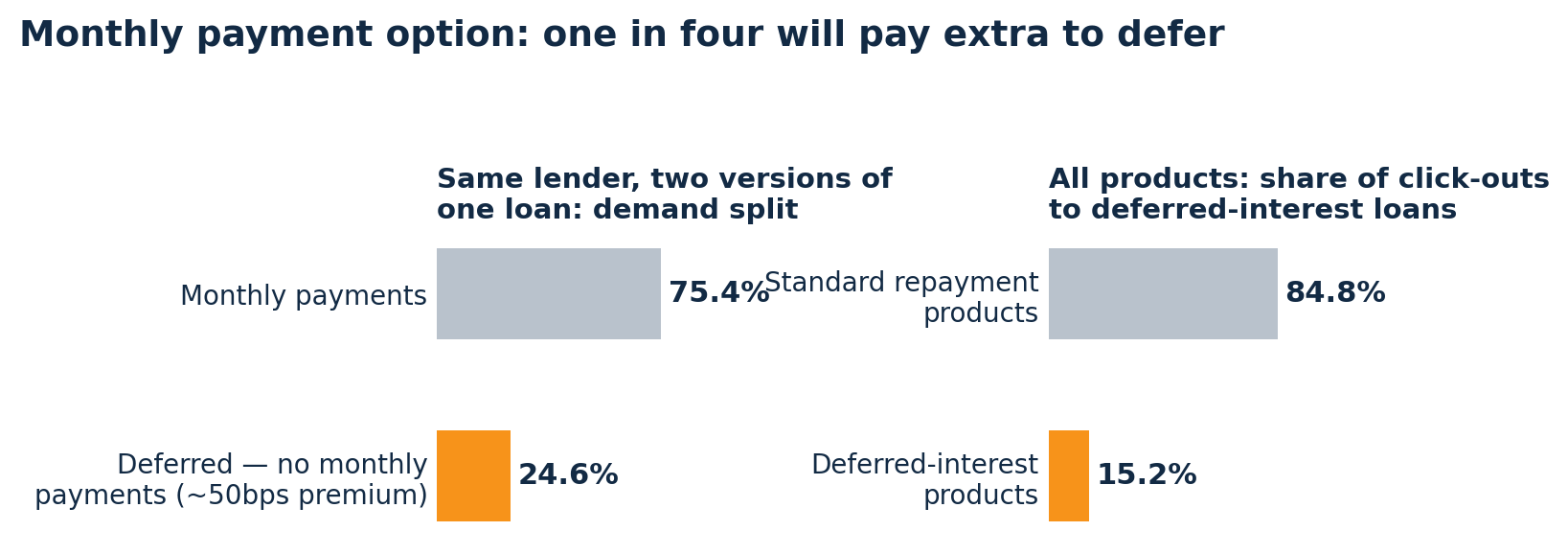

Monthly payment option: one in four will pay to defer

The cleanest experiment in the data is accidental. One lender sells two versions of the same loan, same custodian, same LTV cap, same liquidation mechanics, one with monthly payments and one where interest accrues to maturity at roughly a 50-basis-point premium. The deferred version took 24.6% of that lender's demand.

Across all products, loans with no monthly payments drew 15% of click-outs. Bitcoin borrowers are collateral-rich and, often, cash-flow-shy. A meaningful minority will pay real basis points to keep the monthly cash in their pocket.

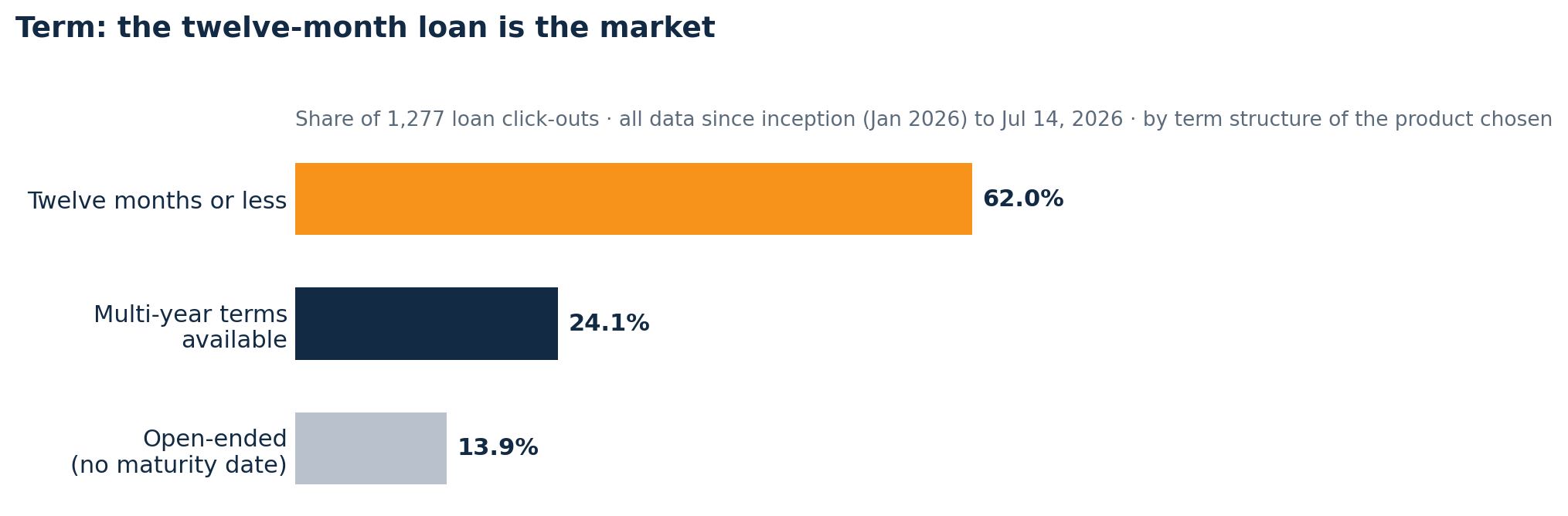

Term: twelve months is the market

The 12-month loan is the default unit of this industry, and demand confirms it: 62% of click-outs went to products whose core term runs a year or less. Products offering genuine multi-year menus, terms from one to five years, drew 24%. Open-ended credit lines with no maturity date took the remaining 14%.

The picture is coherent: borrowers treat these as bridge instruments, not mortgages. They want a year of liquidity against coins they intend to keep.

| Term structure | How it works | Click-outs | Share |

|---|---|---|---|

| Twelve months or less | Fixed maturity; renew or repay at term | 792 | 62.0% |

| Multi-year terms available | Menus running one to five years | 308 | 24.1% |

| Open-ended | Credit-line structure, no maturity date | 177 | 13.9% |

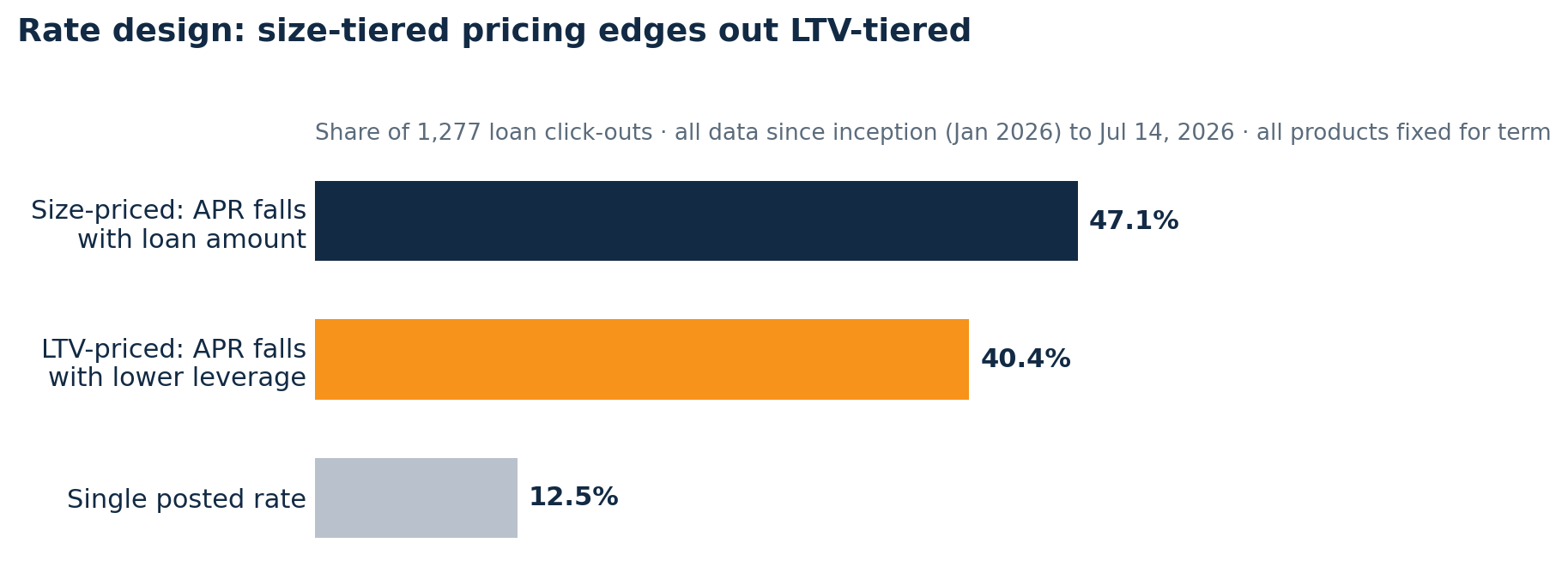

Rate design: fixed, priced by size, and a mispricing

Every product in the click data carries a fixed rate for its term; this funnel compares CeFi lenders, where fixed is the norm. The real split is architecture. Products that tier APR by loan size, bigger loan and lower rate, took 47% of demand. Products that tier by LTV, less leverage and lower rate, took 40%. Single-rate products took 13%.

Here is the tension worth watching: the typical calculator request implies conservative leverage, roughly a quarter of collateral value, and LTV-tiered products are the only ones that pay borrowers for that conservatism. Yet nearly half of demand flows to size-tiered pricing that treats a cautious borrower and a maximally levered one identically. Either borrowers have not noticed, or the discount has not been made loud enough. There is share available for whoever prices conservatism first and says so.

Methodology

Source: first-party events on borrowonbitcoin.com from inception (January 2026) through July 14, 2026. Sample: 515 calculator submissions and 1,277 click-outs to the ten Bitcoin-backed loan products we track (mortgage-product clicks excluded). Bot and internal traffic removed; bots accounted for roughly 47% of raw clicks. Feature shares are revealed preferences: each click-out is attributed to the published attributes of the product chosen, per the BoB Lender Directory (verified July 9, 2026). They are not per-feature filter selections or survey responses. One product offers both a monthly-payment and a pay-at-maturity variant behind a single destination; its clicks are counted as standard repayment, which makes the deferred share conservative. Figures are directional and rounded; percentages may not sum to 100 due to rounding.

About Borrow on Bitcoin

borrow/on/bitcoin is an independent comparison publisher (Sypher Capital Management), not a lender or financial advisor. Data is free to cite with attribution and a link: borrowonbitcoin.com/data.